For those watching the market this past week it might have felt like a white-knuckle rollercoaster ride. The market experienced two drops of more than 1,000 points and then rebounded twice by more than 300 points, each during just one week. Talk about volatility! Market fluctuations like this can cause a range of irrational reactions like, “Get me off this ride!”

Left to our own emotions we can often make regretful financial decisions. A more grounded perspective is in order. For this brief blog post, let me speak to the average American investor who has his or her retirement savings in a 401k, 403b, 457, IRA, brokerage account, etc… Those without pensions have likely been logging into their online statements every few hours and freaking out, wondering what to do.

Remember one very important rule regarding managing pre-retirement assets. Your proximity to retirement matters, so be sensitive to your pre or post retirement timeline before making rash decisions. In addition, each person’s financial chess board is different, so broad brushing any advice would be inappropriate, but some helpful guideposts can calm your jitters.

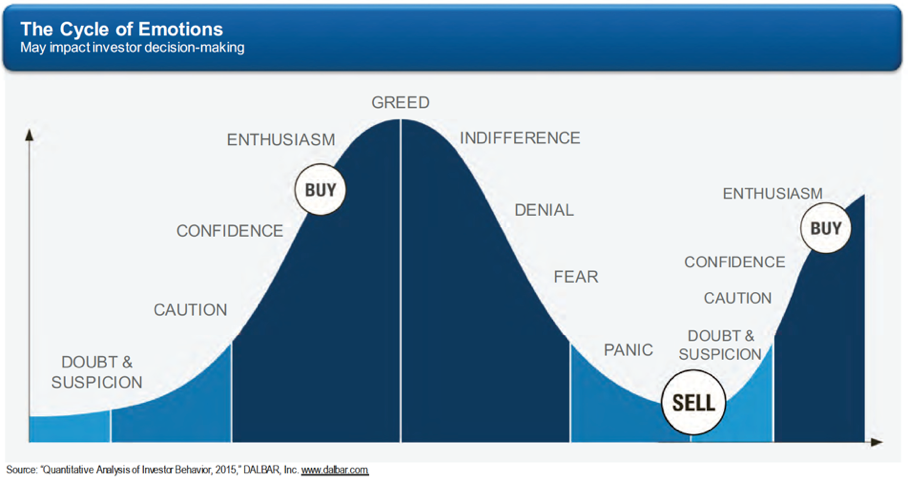

One can experience a wide range of emotions when the markets race up and down. This often can cause “buying” and “selling” decisions at the wrong time. Take a look at the chart below and consider the matching of our emotions with these less than smart “buying” or “selling” decisions.

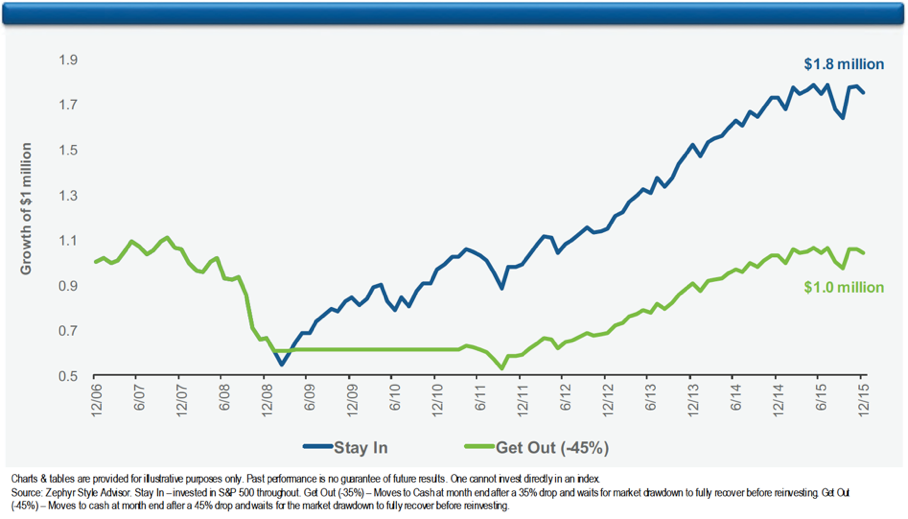

This can obviously translate into entering or exiting the market at the wrong time. Of course, trying to guess market timing is ill advised. It’s best to have a long term strategy and stick with it.

Consider the missed opportunities experienced by many who exited the market in 2008 only to reenter in 2011.

So, how do we calm our nerves when experiencing market jitters like this past week. Consider three simple questions as you make key decisions regarding your long-term retirement savings.

First, what’s the money for?

This may seem a bit basic, but asking yourself this question is essential to bringing a sense of clarity to investment choices. What is the purpose of your invested money? If you can’t identify its purpose then you can’t position it properly.

For many pre-tax accounts, the purpose of the money is, “for retirement.” If you’ve attended one of my Retirement Income Planning workshops then you will know that the answer is more accurately, “for an income stream in retirement.” Just in case you think those are the same ends, they are not! But, for our simplistic discussion today, your invested dollars are promised to the future. You know that day when you want to tell your boss that you have this terrible eye disease and just can’t see coming into work anymore.

If you are in your 20’s, 30’s or 40’s and even up to 10 years before retirement then your investment decisions should reflect a longer-term strategy. Don’t knee jerk every time the market pitches up or down. Decide on a growth strategy and stick with it! The balances will fluctuate, but if you believe in America then position yourself to take advantage of our capitalistic system. Over the long run, expecting an average rate of return of 6-7% per year, adjusted for inflation, is not unreasonable.

In addition, put away as much as possible taking advantage of any available 401k match. It’s free money, so don’t pass it up. A standard rule to save 15% of pre-tax income per year is a good target. If you can’t do that much then work toward it. This is money promised to the future, so get a plan going and stick to it.

Second, what’s the big picture?

Stand back from the forest and look at the big picture. Typically, when we see the dramatic shifts in the markets, it’s often due to something significant happening on the national or world stage. Consider the end of the dot com bubble in the late 1990s, the tragedy of 9/11, or the mortgage backed securities scam and resulting real estate melt down of 2007. The point is that markets often adjust because of significant macro events, but more predictably they also tend to follow important foundational key macroeconomic indicators.

Clearly, this past week’s volatility is not a result of any particular single event, other than a healthy correction to a market being ahead of itself. I know it’s more complicated than this because the 10-year treasury is tracking up and some concerns exist regarding inflation, but given our history these indicators, at least so far, are not out of line. Basically, the markets are just overly excited after eight anemic Obama years.

Of course, if you watch cable news the sky is falling. Our political environment has never been more vial and polarizing, but current economic fundamentals look great. For example, unemployment continues to be very low, interest rates remain attractively low, corporate earnings continue to outperform expectations, consumer confidence is way up, personal earnings are starting to rise, the housing market is doing well, regulatory burden has eased and evidence of positive economic activity is already being felt from the recent tax reform.

So, what is the point? Standing back and taking a big picture view can inform our decisions. This perspective can be helpful in all areas of life. When we get too deep in any micro we can often make mistakes. A macro view will always pay dividends.

Third, who are you listening to?

I was at the dentist this past week and one of the hygienists said her husband was in a panic and moved all his 401k money to cash due to the high volatility. I asked her why. She shrugged her shoulders. She noted they were in their early 40’s. Obviously, this person with over 20 years till retirement doesn’t understand the basics of dollar cost averaging or prudent investing.

While speaking out of state last year, one of the attendees said he had moved all his retirement accounts to cash prior to the 2016 election. His rationale was rooted in his distaste for our current president. He is still out of the market and kicking himself each day because as we know, the markets soared post-election and are still higher than the closing bell last Friday. For this person, political personalities have gotten in the way of sound decision making.

The question, “who are you listening to?” is profound. Rumor, opinion and hearsay are the lowest forms of intelligence. For private sector workers, you live in a Y.O.Y.O. economy. This means You are On Your Own! Private sector defined benefit pension plans are all but gone. In the last 30-years they have been replaced with defined contribution plans like a 401k. These two retirement vehicles couldn’t be more different. One provides a guaranteed source of lifetime income in retirement, while the other is just a pre-tax pot of money where you must figure out how to not run out. It’s time to make education job #1!

For many, your only source of information maybe your Human Resource department. News Flash! They are not financial professionals. In short, many make investing and financial mistakes because they simply don’t understand the basics. At the least, find a trusted advisor who has the heart of a teacher and don’t listen to your broke friends. Learn to cultivate a broad spectrum of inputs into your decision-making process. Finally, make a commitment to education and invest time in your own financial well-being.

Understanding the purpose of your assets, standing back to look at the big picture and securing a trusted source for good financial information is essential to an early claim on financial peace. I hope these questions have given you some context amidst our recent roller coaster ride.

Of course, there is much more to learn! Consider a recent post titled, “10 Principles for Financial Peace”

Enjoy the ride!

I am just a guy who loves life, my wife, my family, my God and my country. I want to pay it forward and make a positive contribution inspiring others to make great life decisions. Growing McKell Partners, a full service wealth management and financial planning practice, is also my passion.

I love a great game of golf, tennis or chasing the sunset on my Cannondale. An evening convertible ride and a bowl of Haagen Dazs peanut butter chocolate ice cream are my go-to stress relievers.

I am just a guy who loves life, my wife, my family, my God, and my country. I want to pay it forward and make a positive contribution inspiring others to make great life decisions.

I am just a guy who loves life, my wife, my family, my God, and my country. I want to pay it forward and make a positive contribution inspiring others to make great life decisions.